Last week we noted that Oregon State Treasurer Ted Wheeler agreed with the Washington State Treasurer that the toll revenue projections for the CRC were unrealistic.

Let’s dig a little deeper into the report (PDF, 695K), as there are quite a few salient points:

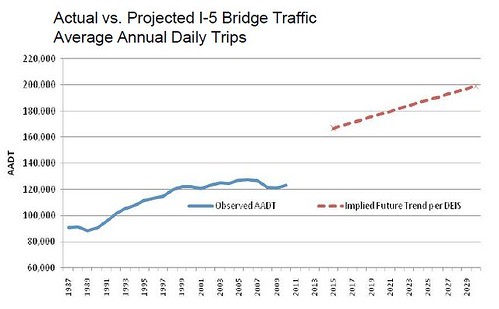

- Traffic projections in the 2008 DEIS are based on a 2002 Metro employment forecast, so they are severely out of date.

- An “investment grade” traffic and toll revenue forecast prior to the initial sale of toll bonds is essential.

- Regardless of whether we issues “toll bonds” or “general obligation bonds”, ODOT and the State General Fund are ultimately on the hook if toll revenues are insufficient to cover bond repayments.

- Overall, the Treasurer believes that a responsible forecast of toll revenues would be 15-25% lower that the current ODOT estimate.

- The project assumes that toll rates will increase 2.5% annually, but experience in the Puget Sound area has shown that it is politically difficult to increase tolls as quickly as planned.

- Between lower traffic volume and more slowly increasing toll rates, the Treasurer estimates there is a gap of $468 to $598 million in project funding.

- The Treasurer suggests several strategies to reduce the funding gap:

- Begin tolling before project completion – potentially worth up to $200 million.

- Use a Federal Transportation Infrastructure Finance and Innovation Act (TIFIA) loan instead of bonding to capitalize toll revenues. This would require congressional authorization but provide for lower interest rates (saving $194 to $238 million) and take the State General Fund off the hook.

- The State “equity” contribution (the portion not funded by tolls) of $450 million would require a 1.5 cent increase in state-wide gas taxes to cover 25-year general obligation bonds. This must be enacted by the Legislature (and while the Treasurer does not point this out, would be subject to referendum).

- The Treasurer suggests that as an alternative, ODOT could issue 12-year “GARVEE” Bonds, but as I understand it these can only be repaid with future Federal funds, which I assume means committing Federal funds that would otherwise be used for other projects.

- Regardless of the toll financing mechanism, the CRC governance “must include a robust toll-setting mechanism to assure that all toll-related debt service is pad in full each year through toll revenues.”

15 responses to “Digging into the Treasurer’s CRC Report”

Or they could just build a highway bridge and not need tolls.

Thanks

JK

Doubtful at best.

Would they be able to do a basic $1 billion bridge without tolls? Even a basic 10 or 12 lane bridge would need new spans north and south of Hayden Island, and new interchanges at Marine Drive, Hayden Island, and SR-500.

They might be able to do a basic $400 million bridge without tolls, although that would require (at a guess) another $200 million or so for a second crossing south of Hayden Island and interchange work at the north end. But a bare-bones version of this project (new freeway bridge, with everything else delayed) could be brought in well under a billion dollars. If the feds kick in half, both Oregon and Washington could pitch in (at most) $200 billion each, and if you add in a smattering of local funding from cities, counties, regional transport agencies and ports, then — conceivably — it could all be done without tolls.

But it also could be done WITH tolls, and be paid off with a fairly modest toll (say, $2) over thirty years or so, even assuming no growth in traffic volume. Personally, I prefer tolls — they can pay for the bridge AND be designed to help manage peak congestion.

Is there any real world evidence that peak tolling works any as advertized? Other than a few percent reduction?

Are a significant number of people really willing shift their schedule to save a dollar or so? (Other than poor people who always seem to get screwed by the local progressive government.)

Thanks

JK

I would rather see the N/NE Quadrant Project (Rose Quarter bottleneck) tackled first.

That way there is even LESS money for the CRC project than there is now!

I would rather see the N/NE Quadrant Project (Rose Quarter bottleneck) tackled first.

I agree. (Devils and details notwithstanding.)

When we have an obvious bottleneck right in the middle of the network, it doesn’t make sense to expand capacity further out before that bottleneck gets fixed.

(And while one person’s “bottleneck removal” is another’s “massive capacity expansion”, I think that a majority of transportation folk can at least agree that I-5 and I-84 close-in feature a lot of unnecessary merges, lane-swaps, suddenly disappearing lanes, closed off local streets, ramps too closely spaced, etc.)

In any case, the right kinds of Rose Quarter bottleneck fixes are far more justifiable than the CRC as currently proposed.

(And while one person’s “bottleneck removal” is another’s “massive capacity expansion”, I think that a majority of transportation folk can at least agree that I-5 and I-84 close-in feature a lot of unnecessary merges, lane-swaps, suddenly disappearing lanes, closed off local streets, ramps too closely spaced, etc.)

Not to mention mystery ramps to nowhere.

Don’t expect the Rose Quarter bottleneck to be addressed.

That represents probably the most logical area that needs expansion.

It’s just like this entire multi-million dollar auxillary lane expansion on 217 to Sunset Interchange.

That area rarely has congestion — most of the congestion is east of there where 3 lanes turn into 2 lanes!

Use your heads, engineers!

It would make sense 3-waying more of 217 instead of building large unnecessary exit ramps and shoulders.

Not to mention mystery ramps to nowhere.

Scarcely a mystery, at least to those of us who have been here a long time. I remember when they all went somewhere. You used to be able to get onto 84 straight from the Steel Bridge, or to exit 84 straight to Union Avenue (now MLK). Sometime around when MAX went in, a whole bunch of ramps on and off I-84 were taken out.

FYI, the mystery ramps at the east end of the Marquam Bridge were to interchange with the Mount Hood Freeway.

Some of the old ramps can be seen in the historical imagery in Google Earth. I haven’t looked too recently, but I think some of them would have interfered with MAX as well as being really close to other ramps.

The big problem with 217 is the short distances between ramps. Fixing that would either require a) closing certain ramps, b) combining more ramps, or c) building braid ramps or collector/distributor lanes.

Or lowering the speed limit on 217 (rebrand it as a “parkway”) so that the shorter distances are less hazardous. Kindasorta works for the city of Bend…

The big problem with 217 is the short distances between ramps.

Do you drive 217 at rush hour? That freeway is underbuilt. I know the transportation dept said that the ramps being too close together is the problem. No, the problem is that 217 is the only north south route on the entire westside. There are no easy alternatives. The freeway either needs to be widened or alternative routes built.

I think 217 is a great candidate for a set of HOV lanes. 2+ passengers should be sufficient, given the driving habits out there. They also need to replace WES with a MAX line at some point in the distant future.

Thanks Doug K. for the history lesson, didn’t know the bit about 84.